The No-Nonsense Guide to Budgeting for Beginners

5 min read

Let’s face it, there are many things we’d rather be doing in our spare time instead of budgeting. It’s not very fun, no matter how old you are. But it’s necessary and, if you do it right, can change your life in the best way.

Knowing exactly where your money is going gives you more autonomy and empowers you to take charge of your life and your future. You know, all that very worthwhile jazz.

If you’re new to budgeting, it can be kind of overwhelming. What’s the best type of budget to follow and am I doing it right? We hear you. If you’re looking for where to start with your budget, you’ve come to the right place.

Will it change your life? We can’t make any promises, that’ll be up to you. But we can help you get the cogs turning towards a better financial future. Here’s our beginner-friendly, no-nonsense guide to budgeting.

The No-Nonsense Guide To Creating a Budget That Works

Why should I create a budget when there’s already an app for it, or 12? Fair question. We’re all about making life easier with tech and if you want to get an app, go for it! But it pays (literally and figuratively) to actively take a good look at your spending habits, beyond inputting numbers and occasionally checking updates in an app.

It can be the kind of shock therapy you need to kickstart the process of changing. Seeing how much you spend every month on everything staring you plain in the face can push you to be more budget-conscious throughout the month.

Even if you go for an app, sitting down and actively engaging with your money habits at least once can offer valuable insight into your lifestyle as a whole. Put in a bit of work now and the dividends will pay off later, we promise.

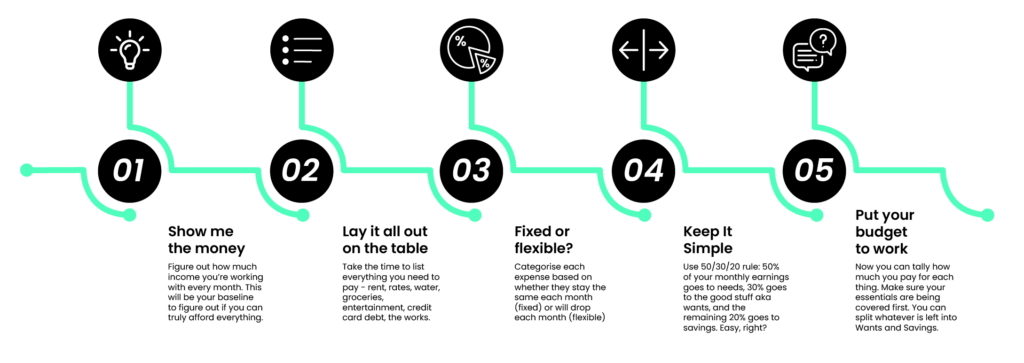

Step 1 – Show me the money

The first step you need to take is to figure out how much income you’re working with every month. If you’re a PAYE employee, then use your net income amount after your tax has been deducted. If you freelance or work as an independent contractor then you’ll need to use your gross income amount because you’ll need to pay your provisional tax.

If your monthly income varies month to month, take a look at your monthly earnings over the past year as a reference and use the amount where you earned the least. Basing your budget around this ensures you cover all your necessary expenses even in the worst-case scenario.

The best part? All the months where you earn more will give you more wiggle room for redistributing that sweet, sweet surplus however you like. As Will Ferell so aptly put it “So many activities!”

Step 2 – Lay it all out on the table (your expenses, that is)

Now’s the time to get serious about everything you spend your money on per month, no matter how embarrassing it might get. We totally get it. We’ve all got little spending skeletons in our closet we’d rather not face, but this only works if you’re 100% honest with yourself. Take the time to list everything – rent, rates, water, groceries, entertainment, credit card debt, the works. The more you go down the rabbit hole, the more comprehensive and useful your budget will be.

Step 3 – Fixed or flexible?

With all your expenses out in the open, you can categorise them based on whether they’re fixed or flexible expenses. Fixed expenses remain the same every month and flexible expenses will dip and drop each month. Rent is generally fixed as is monthly insurance, car repayments and credit card payment instalments. Flexible savings can include water, electricity, groceries, drinks at the bar, dining out and so on.

Step 4 – The KISS principle

You’re nearly there, kudos! With your expenses listed out you’ve got a clear view of where your money is going each month. Now the fun can really begin. At Spot, we like to keep things simple.

There are multiple budget styles out there and we could wax lyrical about the pros and cons of each, but instead, we recommend the 50/30/20 rule or the KISS principle. It goes like this: 50% of your monthly earnings goes to necessary expenses or needs, 30% goes to the good stuff aka wants, and the remaining 20% goes to savings. Easy, right?

Take another look at your fixed and flexible expenses. Chances are most of your fixed expenses will fall into the “Needs” category, but a few flexible ones like groceries and electricity are Needs too.

Most of your flexible expenses will fall into the “Wants” category (we know it’s tempting to list getting a massage or eating out as Needs, but they’re not. Try to think in terms of life or death when it comes to listing Needs).

A great thing about the Spot app is you can create nifty accounts for Needs, Wants and Savings and allocate your money accordingly, but we digress.

Step 5 – Put your budget to work

With your expenses neatly and accurately accounted for you officially have a budget template, cue the confetti.

Now you can tally how much you pay for each thing if you haven’t already (use the previous month’s expenses as a starting point). Then do the math. Do your Needs add up to 50% or less of your monthly income? Do your Wants add up to 30% or less? Only you know.

If the answer is yes, you’re off to a great start! If not, don’t be too worried. Take another look at your Needs and Wants lists and try to figure out where you can do a little trimming. Maybe it means paying off what you owe on your credit card and closing the account if it’s too tempting, or swapping a few nights out for Netflix and chill.

Yes, it means less fun, but running out of cash midway through the month and living on dry crackers for weeks is way worse. Make sure your essentials are being covered first and redirect money if necessary.

You can split whatever is left into Wants and Savings. Here you can really start thinking about some long-term financial goals. Maybe you want to buy a house one day, or take a well-earned trip at the end of the year?

Whatever it might be, start planning now. If you have big goals, it’s worth discussing them with a financial planner. You may need to put away more than 20% in this case, which will either need to come out of Wants, or you’ll need to look at supplementing your income. Hey, it’s all about the side hustle these days, right?

Consistency is Key

Keep tracking your monthly expenses, whether it’s manually or using an app. Either way, the more you track, the more you’ll want to track, and soon enough it’ll practically be second nature. Circumstances change, and you may need to revisit your budget template every few months to make some updates, so have it on hand for reference.

Remember that your budget needs to work for you, not the other way round. It shouldn’t be a straight jacket keeping you from having fun, but rather a guide to help you have fun with a healthy dose of financial responsibility.

Sometimes you’ll have great months, other times you’ll slip up and spend more than you meant to. It happens to all of us. Just aim to do better next month and keep working from your budget.

There you have it. No-nonsense, no fuss. Just a plain and simple budget crash course. Keep your eyes peeled as we drop more money hacks and how-to guides.

The content provided in this article is provided as general information. It is not intended as nor does it constitute financial, tax, legal, investment, or other advice. We accept no responsibility from any loss arising as a result of your reliance on information contained in this article, any related communication or on our app.