Wealth Building for Beginners: Tips for Building Wealth Anyone Can Follow

5 min read

Getting rich when you’re not a Kardashian might seem like mission impossible. Especially when it seems like those who’ve tapped into the millions have either inherited it or traded Bitcoin a couple of times on the stock exchange.

Though it’s a lot less glamorous than that, the truth is anyone can build an impressive nest egg without an inheritance or learning the rocket science behind trading. All you need is a solid plan and a commitment to making it happen. That means no more screenshotting and hoping, but applying and doing.

We’re about to share some of the secrets to building wealth, even if you’re starting from the bottom. So, keep reading.

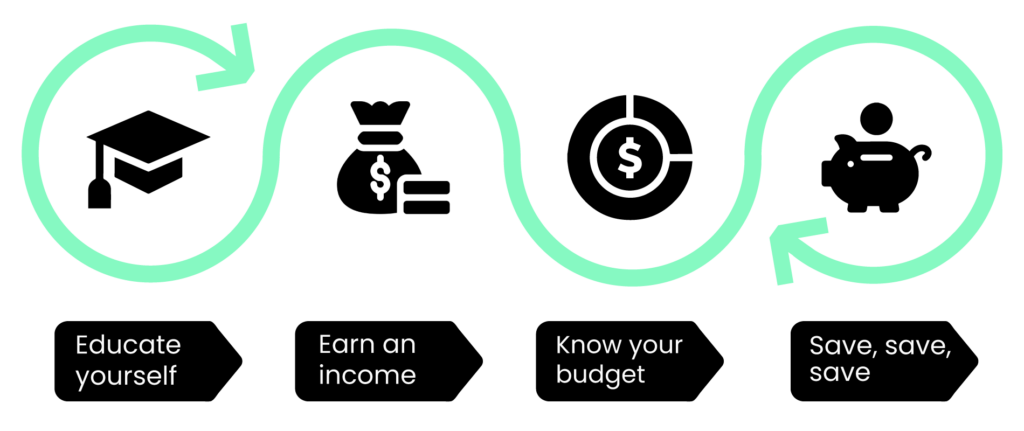

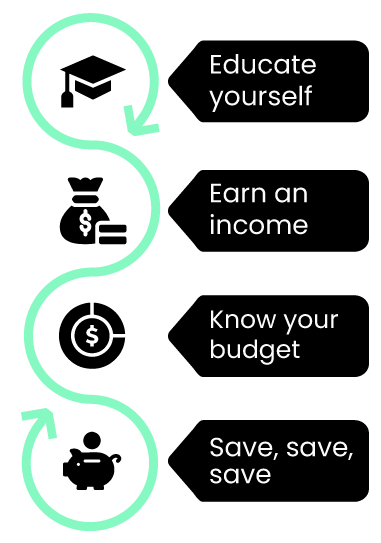

Secret 1 – Educate yourself

To be the next Elon Musk, you first need to change the way you see money.

In his book, Rich Dad, Poor Dad, Robert Kiyosaki said, …” you must invest time in your financial education to build an ark with a solid foundation.”

With that in mind, educating yourself on money isn’t quite like the education you’ve already had in school that ends once you get the Diploma/Degree/Master’s/PhD. It’s ongoing and will require that you apply yourself. Read books on wealth and wealth management. Better yet, subscribe to financial podcasts and Youtube channels and take courses.

Here are a few people you can follow right now, to get 10x smarter about money:

- Robert Kiyosaki is an American businessman and author who grew up with what he describes as a rich and a poor dad. By comparing how they viewed money and investments, he wrote the bestseller Rich Dad, Poor Dad (a book you seriously need to read!). Since then, he’s written more than 26 books on finance.

- Dave Ramsey has a podcast called The Ramsey Show where he engages with his audience on topics around money. As an American personal finance personality, his books on wealth and wealth management have changed many people’s outlook on wealth creation.

- Beth Kobliner’s New York Best Seller, Get a Financial Life: Personal Finance in Your Twenties and Thirties will empower you to get out of debt and live financially free. Her youtube channel, on the other hand, has the potential to educate and entertain both you and your toddler.

Secret 2 – Earn an income

It seems pretty obvious, doesn’t it?

But I guarantee you there’s someone out there daydreaming about flying first class to the Bahamas without a job to save towards it. To that person, we suggest starting your wealth journey by generating a steady income.

Getting rich quick, as appealing as it sounds, often does more harm than good. To create sustainable wealth, you need to have a long-term strategy that shouldn’t include get-rich-quick anything.

Brian Tracy, a self-development guru lives by the notion that adding value is the foundation of wealth creation. From that perspective, no matter how you intend to get a stable income, think of ways to add value and watch the money roll in.

Secret 3 – Know your budget

99% of the time wealth is built, not inherited. Earning a steady income isn’t enough – you also need to live within your means, even if it means fewer nights out on the town, to make those jetsetter dreams a reality one day!

A budget, in which you outline and monitor your income and expenses, is the best way to manage the stable income you shall or do have.

The 50:30:20 rule is a popular budgeting technique. 50% of income goes to essential expenses like rent, 30% to non-essentials like those shoes you’ve had an eye on, and 20% to savings and investments.

When you first create your budget it’s going to look like a financial diary. After some time though, you should have a picture of where your money goes on a month-to-month basis, helping you to make wiser decisions.

Secret 4 – Save, save, save!

Saving isn’t particularly fun, especially when there are so many other things you could be doing to enjoy your hard-earned cash! It’s the key to unlocking long-term wealth though – and the more you save each month, the sweeter the returns will be one day. The 50:30:20 rule is a popular guideline to saving that suggests you should be putting away at least 20% of your monthly earnings into investments or savings accounts. It’s not a hard and fast rule but can be a useful benchmark for assessing just how much you can afford to put away once your fixed expenses are accounted for. Give it a try and you may be surprised at how much moola you end up recuperating by cutting a few things out and putting your money where it will really count.

Conclusion

Following these tips won’t guarantee a change of address to the Hamptons anytime soon, but they could one day. By practising the habit of delayed gratification, you increase your savings and investments so one day you can sit back, put your feet up, cocktail in hand, and reap the benefits of making good decisions while you were young!

The content provided in this article is provided as general information. It is not intended as nor does it constitute financial, tax, legal, investment, or other advice. We accept no responsibility from any loss arising as a result of your reliance on information contained in this article, any related communication or on our app.