Good vs Bad Debt - Is there really a difference?

5 min read

Good debt sounds like an oxymoron doesn’t it? Like, when did debt become a good thing? Especially when almost every financial expert we’ve heard has taught that the first step to getting rich was annihilating all forms of debt. Quickly and without remorse.

With time, society has changed its view on debt having realised that not all debt is bad and that having certain kinds of debt can actually be beneficial. However, understanding the difference between them could either work towards building or tearing down your goal of financial freedom.

This post will help you to Spot the difference between good and bad debt to build the future you deserve!

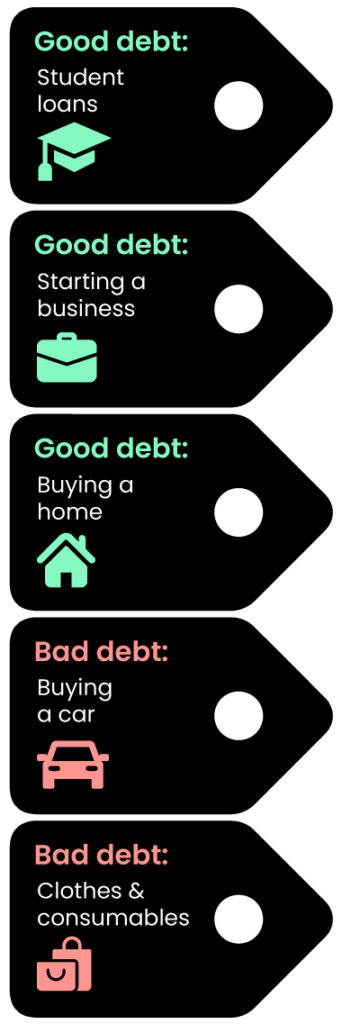

Good Debt

Think of debt as a balancing scale. On the one side of the scale, you have something that appreciates (value increases) or depreciates (value decreases) over time. On the opposite side of the scale is the money you’d need that should justify the loan.

Good debt enhances the quality of your life over time. Balancing both sides of the scale is the goal when acquiring good debt.

Here are a few examples of good debt.

Student loans

Education is an investment that appreciates your value in the marketplace. The more educated you are, the higher your earning potential will be. Don’t have a job yet? Get educated.

Though there may be some exceptions, employers find an educated worker an asset to the team. The biggest benefit to a student loan is that it can be paid off sooner with a high paying job once you’re in the workforce.

That said, not all student loans are worth investing in. Consider both the long and short-term prospects for your field of study that have the potential to create long-term career satisfaction.

Starting a business

If your side hustle has grown into a main hustle, borrowing money to scale is something worth chewing over. Without the financial boost, you may find being the captain of your ship, as amazing and rewarding as it may be, financially taxing.

Weigh the loan against potential risks you may face and if it makes financial sense, take the leap of faith!

Buying a home

By now we’re sure you’ve read or heard somewhere how property is an appreciating asset.

A great number of millionaires have shared that buying a property with a home loan or mortgage to sell it for a profit at a later stage, is how they started accumulating their wealth.

If your goal isn’t to buy and sell property, owning a house has other benefits. Like the freedom of refurbishing the kitchen that came with a 70s vibe you don’t like, or getting tax breaks you wouldn’t get as a renter.

As a property owner, you also have the residential real estate option available to you that allows you to rent your home for someone else to pay your home loan off. This will free you up to acquire more property and grow your wealth.

Bad debt

Unlike good debt which adds value to your life over time, bad debt does the exact opposite.

In essence, it’s about using borrowed money to buy assets that will depreciate or lose their value over time.

Examples of bad debt are:

Buying a car

This may come as a surprise to you but, the moment you turned the keys and drove that shiny new BMW off the showroom floor of the dealership, it depreciated. That’s before you even got the chance to show off to your neighbours. Bummer!

Borrowing money for a car doesn’t make good financial sense.

But what happens when you work across town and desperately need your own wheels? Our advice to you is to look for a deal that has a very low-interest rate so that as your car loses value, you’re not left paying off interest for years to come.

Clothes & Consumables

There’s always a reason to go shopping isn’t there? Moved into a new apartment and the old couches don’t seem to fit with the colour scheme? The dog chewed a hole into your favourite shoes and now you need an entirely new wardrobe…It happens. When you get the urge to splurge, we suggest using cash instead of a credit card. The last thing you need is the strain that comes from paying off clothes that will be out of fashion before the debt is paid off.

Conclusion

Something that may seem controversial is the idea of borrowing more to pay what you’re failing to pay off. Though this sounds like a bad idea, it’s not. Debt consolidation, as it’s known, typically has lower interest rates than credit cards do.

All things considered, there isn’t always a hard-set rule when identifying good and bad debt. Having a look at your unique financial situation will help you make the right debt decisions.

The content provided in this article is provided as general information. It is not intended as nor does it constitute financial, tax, legal, investment, or other advice. We accept no responsibility from any loss arising as a result of your reliance on information contained in this article, any related communication or on our app.